ADW Capital Management Sends Letter to Driven Brands Board and Controlling Shareholder Roark Capital Calling on the Company to Immediately Undertake a Strategic Review Process

Contends Driven Brands is Undervalued by the Public Markets due to Structural, Capital Allocation, and Governance Failures

Believes That Strategic Process Will Maximize Value for All Shareholders

Believes Shareholders Can Fetch in Excess of $30 a Share in a Controlled Sale or Breakup

MIAMI BEACH, Fla., March 26, 2026 (GLOBE NEWSWIRE) -- ADW Capital Management, LLC, which owns approximately 2.5% of the Common Stock of Driven Brands Holdings Inc. (NASDAQ: DRVN) (the “Company”), issued an open letter to the Company’s board of directors and controlling shareholder Roark Capital Group regarding opportunities to maximize value for all shareholders and urging the Company to undertake a strategic review process.

A full copy of the letter is below:

March 25, 2026

Board of Directors

Driven Brands Holdings Inc.

440 South Church Street, Suite 700

Charlotte, NC 28202

and

Roark Capital Group

1180 Peachtree Street NE, Suite 2500

Atlanta, GA 30309

Members of the Board of Directors of Driven Brands Holdings Inc. and Representatives of Roark Capital Group:

ADW Capital Management, LLC (“ADW”) is a long-term, research-driven investor focused on unlocking value in misunderstood and structurally mismanaged businesses. We have spent considerable time analyzing Driven Brands Holdings Inc. (NASDAQ: DRVN) (“Driven Brands” or the “Company”), its franchise system, capital structure, and strategic positioning. During this period, we have accumulated an approximately 2.5% stake in the Company’s Common Stock.

Our conclusion is straightforward: Driven Brands is materially undervalued not because of external pressures, but due to self-inflicted structural, capital allocation, and governance failures. We believe that the recent accounting failures, while perhaps small in nature, are a feature of a greater disease. Roark Capital Group (with its affiliates, “Roark Capital”), the Company’s controlling shareholder, appears to be distracted in trying to fix / grow its larger restaurant platforms to get them public for a limited partner base starved of “DPI” and Driven Brands has caught the brunt of this neglect.

Simply put, the current trajectory is untenable and immediate and decisive action is required.

The Core Problem: Driven Brands Is a Conglomerate Without Synergy

Driven Brands today is a loosely assembled collection of automotive service brands that appears to lack meaningful operational integration or strategic coherence but individually could all be very valuable independently or to others.

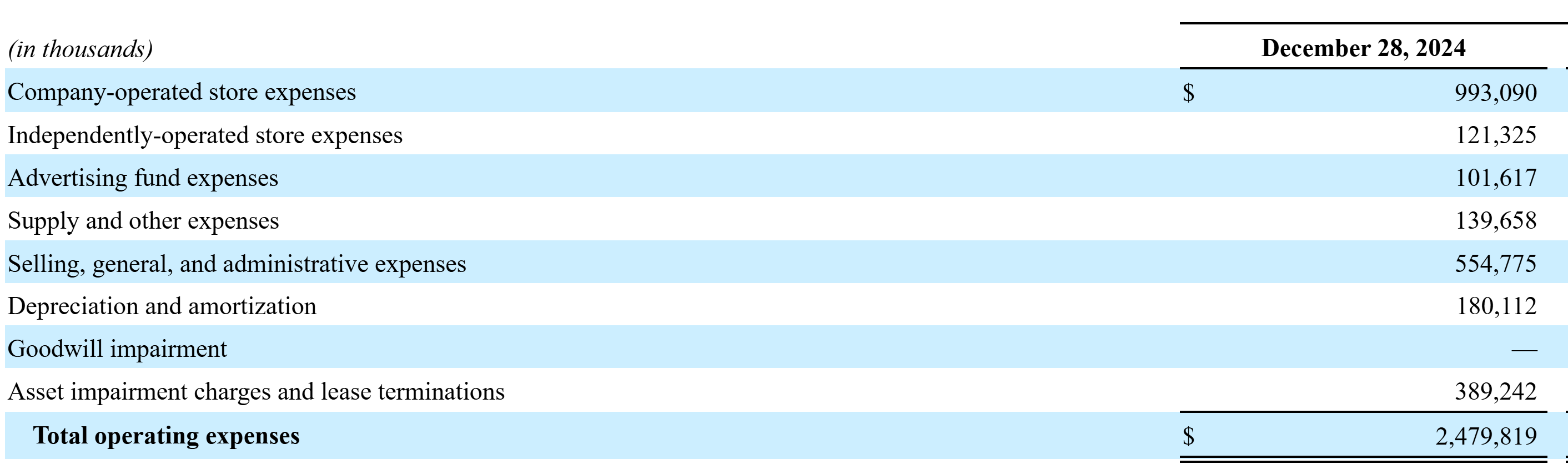

Are there real identifiable synergies across brands or segments? Corporate overhead which is meant to be “shared services” / public company costs seem very high at ~ $160 - $180 mm especially after the car wash disposals1 and compared to peer Holdcos. For reference, corporate G&A was ~$45 mm in 20192. Total SG&A appears to be even more egregious on an absolute basis at ~$555 mm in 20243 and certainly disproportionately high relative to pure play franchise peers and benchmarking we have attempted to do against other corporate owned automotive service peers. See below excerpt from the Company’s 2024 10-K that excludes operating expenses from Company owned stores and franchised stores4 -- meaning this ~$555 mm in 2024 is on top of those expenses!

Is this a platform or is it a holding company that trades at a discount to both well-run franchisors and corporate / asset-heavy operators?

Capital Allocation Has Largely Destroyed Credibility

The Company has pursued an aggressive roll-up / greenfield strategy funded by leverage and subsequently followed up by reversals, divestitures, and restructuring efforts.

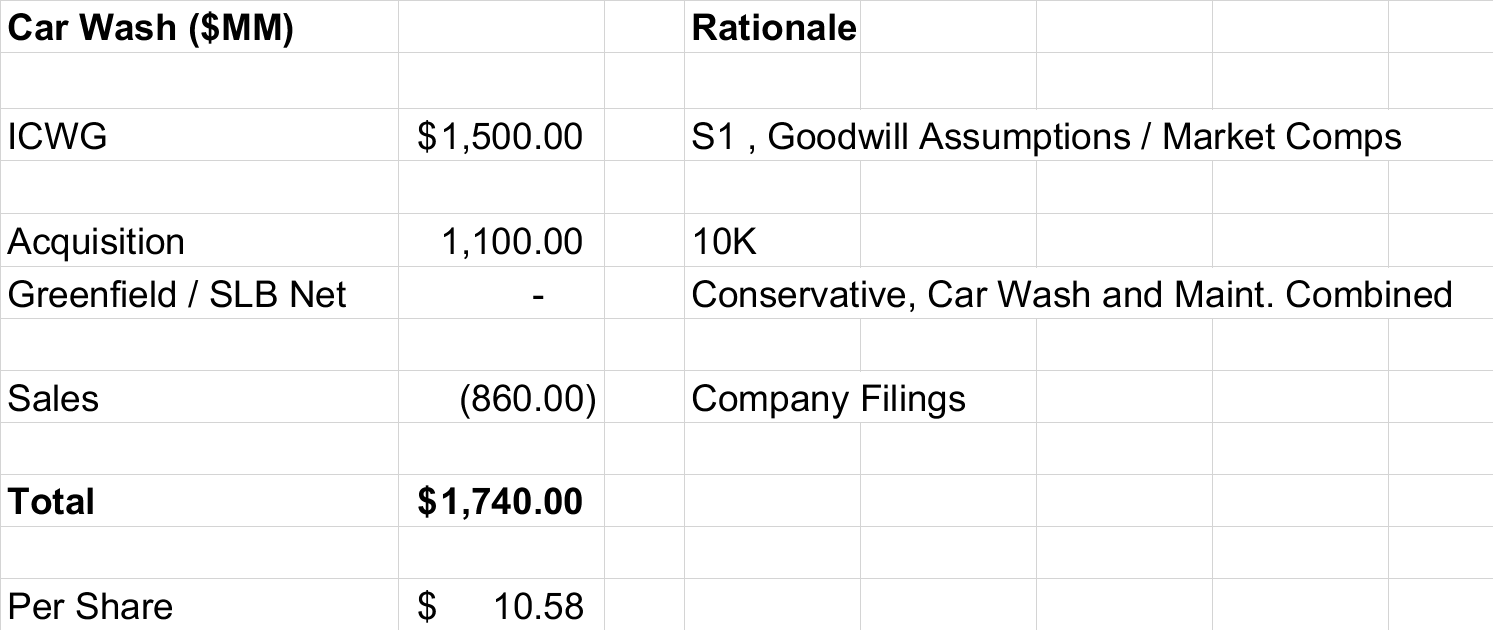

The car wash expansion and subsequent divestiture not only eroded investor trust but also cost Driven Brands’ shareholders meaningful amounts of money. While it is very hard to reverse engineer what exactly the car wash endeavor cost public market shareholders directly, our own internal estimates / triangulation seems to value the International Carwash Business somewhere between $1.4 and $1.6 bn when it was vended into the Holdco pre-IPO.5 While we think there is likely a positive net spend on greenfield, the sale-leaseback proceeds for car wash were commingled with maintenance facilities so we called it a “wash” (generous). When you include the M&A disclosed in the public filings by year and you back out the proceeds from the two divestitures, the Company’s foray into car wash conservatively “cost” shareholders over $1.74 billion dollars or over $10.58 a share, or nearly the Company’s entire market cap today!

Why should investors underwrite heavily adjusted EBITDA narratives, huge cash restructuring charges, and dismal capital allocation like car wash prospectively?

The Only Path Forward: Break-Up or Sale

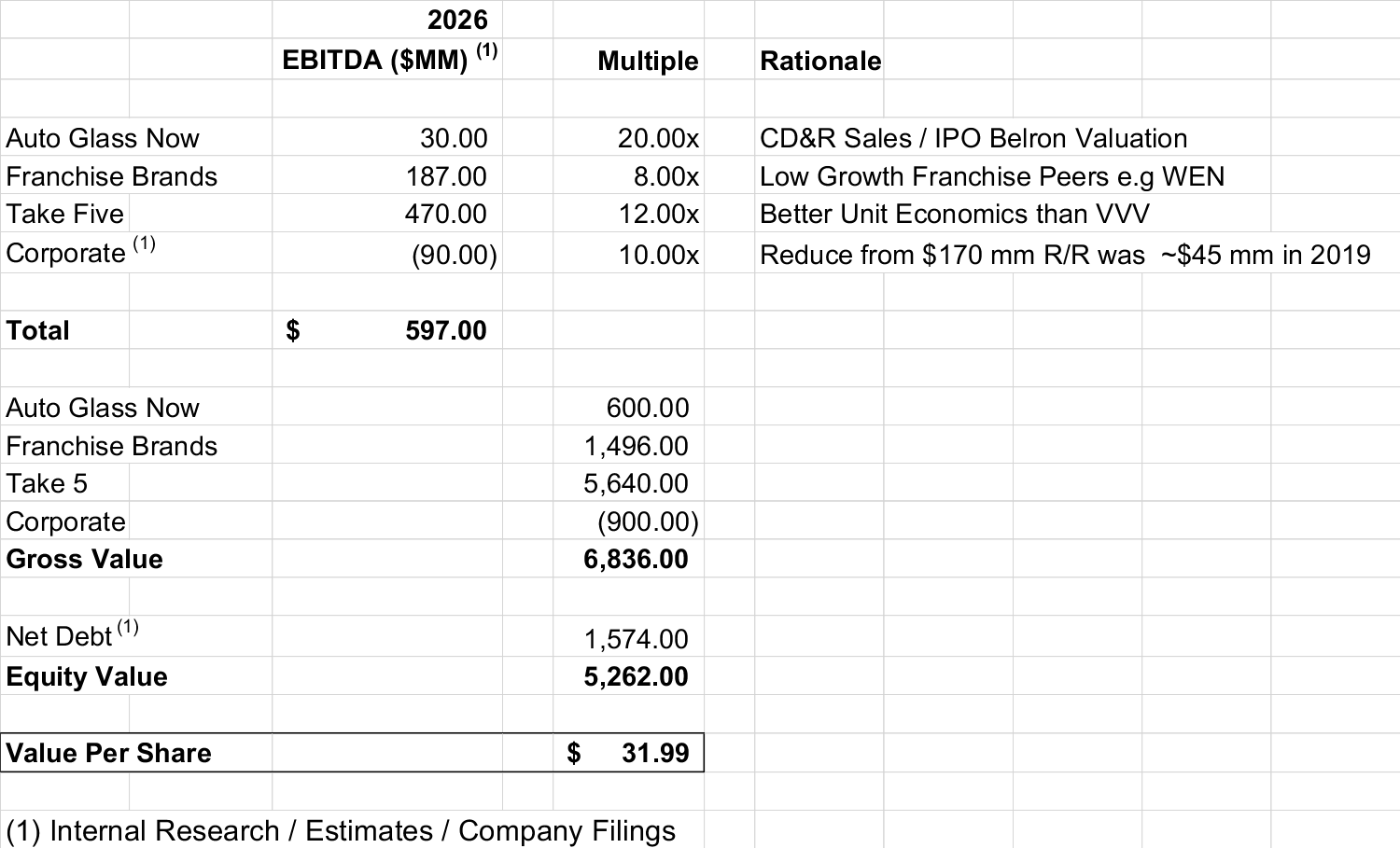

Between the Company’s dalliance in car wash, recent accounting weakness, perceived G&A waste, and Roark Capital’s ownership overhang, we believe investors are just simply fed up. If one looks at our table below, it is easy to comprehend that the value discrepancy placed on Roark Capital’s stewardship of Driven Brands is just too big to ignore.

We believe the highest-value outcome is a strategic separation of assets or a full sale process to a strategic or financial buyer. Given the simplified structure / growth algorithm post car wash divestiture, we believe any number of strategic or financial buyers could acquire the Company in aggregate or each one of its segments could likely be sold for a higher multiple than what the Company in aggregate is trading for today.

If there is any doubt around the value of the Company’s assets it’s that we may be TOO LOW on our SOTP calculation. Why don’t we look to Jonathan Fitzpatrick’s (former CEO of Driven Brands) comment from September 5, 2024 at the Goldman Sachs Global Retailing Conference for reference?:

On September 5, 2024, Driven Brands’ share price closed at $14.22. Using simple inductive reasoning, Jonathan is implying the shares were worth over $42.00 18 months ago!!

What is even more crazy is that Take 5 was a much smaller asset then! Also, if you want to seek to discredit Jonathan Fitzpatrick look no further than his appointment as CEO of Subway as he was “promoted” by Roark Capital to run the asset following their acquisition!

Immediate Actions is Required

We urge the Board to announce a strategic review and engage independent advisors, increase transparency, reduce overhead, and evaluate governance changes. We know Roark Capital is focused on much larger assets in in its private portfolio but why should minority shareholders suffer at Driven Brands? The Company and its Board have a fiduciary duty to all shareholders as well as its limited partners of the private funds where these shares sit.

Driven Brands has valuable assets, but the Company is simply not on a path to realizing that value. The Company must pursue decisive action to unlock this massive disconnect in shareholder value.

Sincerely,

Adam Wyden

Managing Member

ADW Capital Management, LLC

About ADW Capital Management, LLC

ADW Capital Management, LLC is the investment advisor for a concentrated, long-biased investment partnership founded by Adam Wyden in 2010.

Contact

Adam Wyden

ADW Capital Management, LLC

(646) 684-4086

adam@adwcapital.com

______________________________

1 Company Filings / Based on ADW estimates and analysis

2 Company Filings

3 Company Filings

4 Company Filings

5 Company Filings / Based on ADW estimates and analysis

Photos accompanying this announcement are available at:

https://www.globenewswire.com/NewsRoom/AttachmentNg/267cf30d-139e-4c47-a51e-44b606c36320

https://www.globenewswire.com/NewsRoom/AttachmentNg/f4c1a359-cea0-407f-95f4-e57f653bcde3

https://www.globenewswire.com/NewsRoom/AttachmentNg/5460ef24-175f-483c-a43e-32640a642c21

https://www.globenewswire.com/NewsRoom/AttachmentNg/ae305bcc-7f2e-4b91-9291-7a985b8121ae

© Copyright Globe Newswire, Inc. All rights reserved. The information contained in this news report may not be published, broadcast or otherwise distributed without the prior written authority of Globe Newswire, Inc.